Table of Contents:

- Limitations of Marginal Costing

- Marginal Costing Meaning

- Features of Marginal Costing

- Objectives of Marginal Costing

- Scope of Marginal Costing

- Advantages of Marginal Costing

- Disadvantages of Marginal Costing

- Importance of marginal costing

- Characteristics of Marginal Costing

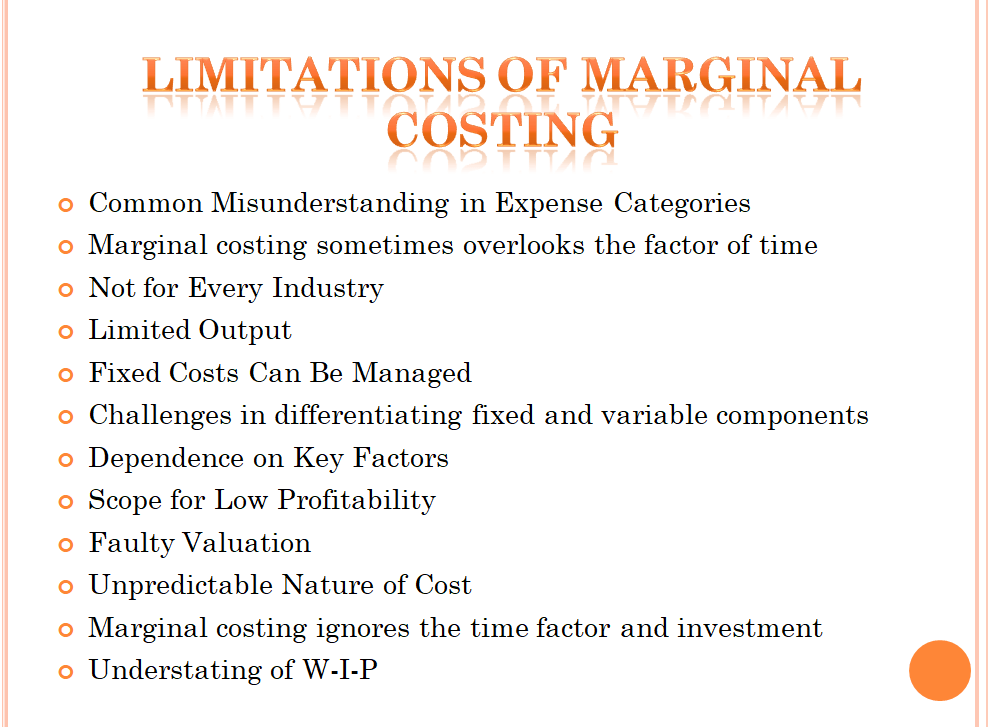

Limitations of Marginal Costing

Marginal costing is a useful tool for decision making, but it has certain limits, therefore businesses need to be well aware of the limitations of marginal costing.

By understanding the limitations of marginal costing and adopting a more suitable approach to cost analysis, they can improve their decision making processes and overall performance.

Limitations of Marginal Costing are as follows:

- Common Misunderstanding in Expense Categories

- Marginal costing sometimes overlooks the factor of time

- Not for Every Industry

- Limited Output

- Fixed Costs Can Be Managed

- Challenges in differentiating fixed and variable components

- Dependence on Key Factors

- Scope for Low Profitability

- Faulty valuation

- Unpredictable Nature of Cost

- Marginal costing ignores the time factor and investment

- Understating of W-I-P

1. Common Misunderstanding in Expense Categories

People often think expenses can be easily sorted as either fixed or variable. However, this simple idea doesn’t consider expenses like employee bonuses, which depend on management decisions and don’t relate to how much is produced or the time taken.

2. Marginal costing sometimes overlooks the factor of time

There are cases where two outputs have the same marginal cost, even if one takes twice as much time to make. However, in reality, tasks that take more time usually end up costing more.

3. Not for Every Industry

Marginal costing doesn’t work well in some industries, like shipbuilding and contracts.

4. Limited Output

There are certain limitations of marginal costing one of which is limited output. Once a certain amount is produced, fixed expenses might unexpectedly increase, so it’s not always reliable beyond a certain level of production.

5. Fixed Costs Can Be Managed

Marginal costing overlooks the idea that fixed costs can be controlled. Using budgetary control techniques can help effectively manage the number of fixed overheads.

6. Marginal costing ignores the time factor and investment

The marginal cost of two jobs may be the same but the time taken for their completion and the expenses associated with the machines used can vary. The true cost of a job which takes a longer time and uses an expensive machine would be higher. Marginal costing does not reveal this fact.

7. Understanding of Work-in-Progress (WIP)

In the context of marginal costing, it is important to note that under certain circumstances, stocks and WIP can be inaccurately undervalued.

8. Challenges in differentiating fixed and variable components

It is difficult to classify the expenses into fixed and variable categories. Most of the expenses are neither entirely variable nor completely fixed. For example, various amenities provided to workers may have no relation either to the volume of production or time factor.

9. Dependence on key factors

The contribution of a product itself is not a guide for optimum profitability unless it is linked with the key factor.

10. Faulty valuation

Overheads of a fixed nature cannot altogether be excluded particularly in large contracts, while valuing the work-in-progress. To accurately reflect the correct position, fixed overheads have to be included in the work-in-progress.

11. Scope for Low Profitability

Sales staff may mistakenly confuse marginal cost with total cost and sell products at a price; which will result in loss or low profits. Hence, it is imperative to inform the sales staff to exercise caution when providing information regarding marginal costs.

12. Unpredictable nature of Cost

Some of the assumptions regarding the behaviour of different costs may not hold in a realistic situation. For example, the assumption that fixed costs will remain static throughout is not correct. Fixed costs may change from one period to another.

For example, salary bills may go up because of annual increments or due to changes in pay rates etc. The variable costs do not remain constant for each unit of output. Price changes in wage rates, raw materials, and other factors may occur after reaching a certain level of output due to material shortages, a shortage of skilled labour, bulk purchase concessions, etc.

Marginal Costing Meaning

Marginal costing is a distinct method of costing like job costing, process costing, operating costing, etc., but a special technique used for managerial decision making. It is used to provide a basis for the interpretation of cost data to measure the profitability of different products, and cost centres in the course of decision making.

Marginal costing is a technique that also divides costs into two categories, but of somewhat different natures. Marginal costing distinguishes between fixed and variable costs as conventionally classified. The marginal cost of a product refers to its variable cost.

The term ‘marginal cost’, derived from the word ‘margin’, is a well-known concept of economic theory. The accountant’s concept of marginal cost differs from the economist’s concept of marginal cost. From the economist’s point of view, the cost incurred in producing an additional unit of product is termed marginal cost.

From the accountant’s point of view, marginal cost applies to the total cost obtained by adding prime cost and variable cost. In other words, all costs other than fixed costs are the marginal cost.

The Institute of Cost and Management Accountants, London, has defined Marginal Costing as “The ascertainment of variable costs and of the effect on profit of changes in volume or type of output by differentiating between fixed costs and variable costs”.

Marginal Costing is also referred to as Variable Costing. It is the change in aggregate costs that occurs when the volume of output is increased or decreased by one unit. This change is measured by the total variable cost associated with one unit.

Features of Marginal Costing

The features of marginal costing are given as follows:

1) It is a technique of analysis and presentation of costs that helps management in making many managerial decisions and is not an independent system of costing such as process costing or job costing.

2) All elements of cost-production, administration selling and distribution are classified into variable fixed and variable. and fixed components. Even semi-variable costs are analyzed.

3) The variable costs also known as marginal costs are regarded as the costs of the products.

4) The profitability of departments and products is determined by their contribution margin.

5) Closing stock is valued at variable cost.

Objectives of Marginal Costing

The following are the objectives of marginal costing:

1) Fixed cost remains constant at all levels of sales and output. As a result, the total cost does not change in direct proportion to the change in output.

2) The inclusion of fixed costs as product costs leads to variations in cost per unit based on different levels of activities during different periods.

3) Once organizations install facilities and commit to fixed costs, they incur these costs regardless of capacity utilization.

4) Fixed costs are identifiable with a particular accounting period. Therefore it is improper to carry forward fixed costs to a subsequent year as part of inventory valuation.

5) Since the level of output and sales does not influence fixed costs, they are irrelevant for most decisions at the operations stage. Determining the minimum price, decisions on dumping, acceptance or rejection of an order, the decision to produce or shut down, decisions regarding product mix, etc., are all guided by variable and differential costs, not fixed costs. Hence, there is a need for marginal costing.

Scope of Marginal Costing

The concept of marginal costing, as explained thus far, includes several scopes, some of which are as follows:

List of the scope of marginal costing:

- Helps in the Prediction of Profit

- Helps in Determining Prices

- Helps in Decision-making

- Helps in Profit Planning

1) Helps in the Prediction of Profit

Marginal costing enables management to predict profit over a wide range of volumes. This knowledge is very useful in preparing a flexible budget.

2) Helps in Determining Prices

During lean business seasons, the company must carefully determine the prices of its products. At times, it becomes necessary to reduce prices to stimulate product sales. For all such decisions, management must assess the impact of price reductions on the company’s profit position through cost-volume-profit analysis.

3) Helps in Decision-making

Analysis of the cost-volume-profit relationship helps in decision making. There are situations when management has to decide whether to increase its capacity or not. With the knowledge of cost-volume-profit analysis, a manager can easily make decisions showing in its report how utilization of available capacity will lead to an increase in profit.

4) Helps in Profit Planning

The cost-volume-profit analysis aids in profit planning. In profit planning, the company first sets the profit it aims to achieve during the ensuing year. Subsequently, efforts are made to determine the sales level required to attain that profit. Cost-volume-profit analysis assists in profit planning in the following ways:

i) It aids in estimating income at a specific sales level.

ii) It helps determine the change in profit due to changes in sales volume.

iii) It facilitates the execution of profit planning. In other words, we can determine the sales level needed to achieve the desired profit by understanding the relationship between cost, volume, and profit.

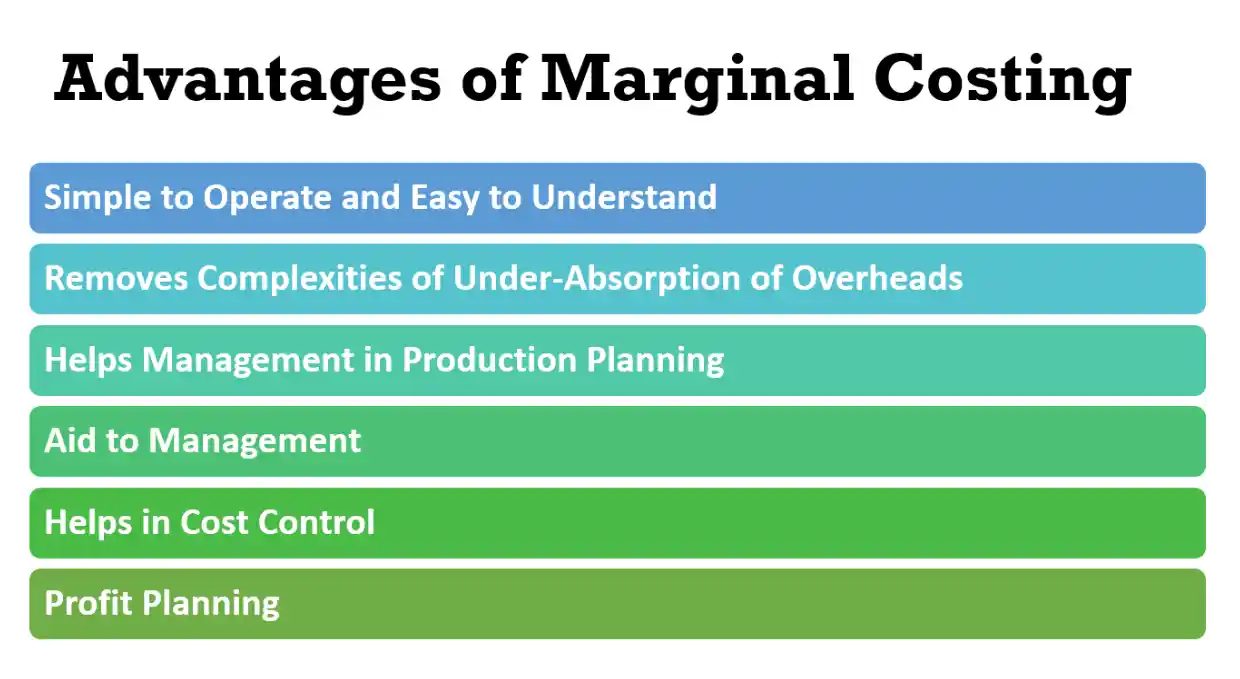

Advantages of Marginal Costing

The advantages of marginal costing are as follows:

1) Simple to Understand and Easy to Operate

The technique of variable costing is very simple to understand and easy to operate. Since fixed costs are kept outside the unit cost; the cost statements prepared based on variable costs are much less complicated.

2) Removes Complexities of Under-Absorption of Overheads

It does away with the need for allocation, apportionment and absorption of fixed overheads and hence removes the complexities associated with under-absorption of overhead costs.

3) Helps Management in Production Planning

Variable cost remains the same per unit of output irrespective of the level of activity. It is constant and helps the management in production planning

4) Aid to Management

It is a valuable asset to management for decision making, fixation of selling prices, selection of a profitable product/sales mix, make-or-buy decisions, key or limiting factor problems, optimizing activity levels, decisions to close or shut down, evaluating performance, and making capital investment decisions, among others.

5) Helps in Cost Control

Since fixed costs are not controllable and it is only variable or marginal costs that are controllable, variable costing, by dividing costs into controllable and non-controllable, helps in cost control.

6) Profit Planning

It helps management in profit planning by analyzing the correlation between costs, volume, and profits. Additionally, break-even charts and profit graphs help to simplify the problem’s complexities and make it understandable even to individuals without a finance background.

Disadvantages of Marginal Costing

The disadvantages of marginal costing are given as follows:

1) Segregation into Fixed and Variable

It is difficult to classify all the costs into fixed and variable with accuracy since some costs have no relation to the volume of output or even the time. For example, management’s decision regarding bonuses to workers may not be directly related to time or output.

2) Apportionment of Fixed Costs

In the case of multiple products, separate break-even points are to be calculated. This presents a challenge in allocating fixed costs to each product.

3) Based upon several Assumptions

The technique of variable costing is based upon several assumptions that may not hold goods under all circumstances.

4) Problems regarding Under or Over-Absorption

Although the technique of variable costing overcomes the problem of under or over-absorption of fixed overheads, problems still exist regarding the under or over-absorption of variable overheads.

5) Unable to Fix Selling Prices

Establishing selling prices in the long term cannot be done without considering fixed costs. Therefore, pricing decisions should not be based solely on marginal cost.

6) Useful Only in Sports Profit Planning and Decision Making

Variable costing is especially useful in short-profit planning and decision making. For decisions of far-reaching importance, one is interested in special-purpose costs rather than the variability of costs.

Importance of Marginal Costing

The technique of Marginal Costing proves immensely useful to management in making various decisions, as explained below:

1. Assists in Selecting Production Lines

The Marginal Costing technique helps evaluate the profitability of different production lines, enabling the selection of the most lucrative ones.

By comparing the profitability of various products, it becomes possible to discontinue unprofitable products or activities and focus on those that yield higher profits.

Additionally, it guides the introduction of new products and aids in deciding the optimum mix of products considering available capacity and resources.

2. Assists in Deciding the Method of Manufacturing

When a product can be manufactured using two or more methods, calculating the marginal cost for each method helps decide which method should be adopted.

3. Helps in Determining Production Volume

Marginal Costing assists in identifying the most profitable output level for an ongoing concern. It optimises production capacity, determining a profitable relationship between cost, price, and volume. This aids management in setting the best-selling price for products, ultimately maximising profit.

4. Facilitates Decision on Whether to Shut Down or Continue

Particularly during periods of trade depression, Marginal Costing aids in deciding whether production in the plant should be temporarily suspended or continued despite low demand for the firm’s products.

5. Aids in Decision-Making for Production or Procurement

Marginal Costing assists in deciding whether a specific product should be manufactured in-house or procured from an external source.

Management can make informed decisions by comparing the external procurement price with the marginal cost of production. If the procurement price is lower than the marginal cost of production, it may be advisable to procure the product externally.

Characteristics of Marginal Costing

The main characteristics of marginal costing are:

1) Treatment of Fixed and Variable Costs: Fixed costs are considered period costs, and variable costs are considered product costs. Consequently, fixed costs are not included in the product cost.

2) Impact of Stock Changes: The difference in the value of opening and closing stock does not affect the unit cost of production, as all product costs are variable.

3) Valuation of Stock: Work-in-progress and finished goods stock is valued at marginal or variable costs.

4) Classification of Costs: All costs are fixed and variable. The variable cost per unit remains constant, while fixed costs remain constant in total, irrespective of changes in production.

FAQs

1. What is marginal costing in cost accounting?

Marginal costing may be described as “the ascertainment of marginal costs and the effect on profit resulting from changes in the volume or type of output, achieved by differentiating between fixed costs and variable costs.” The concept of marginal costing is based on the behaviour of costs that fluctuate in accordance with production levels.

In marginal costing, costs are classified into fixed and variable costs. Even semi-variable costs are analyzed into fixed and variable components. The stock of work-in-progress and finished goods is valued at marginal cost. Marginal cost equals the increase in total variable cost, as within the existing production capacity, an increase in one unit of production causes an increase in variable costs only, while fixed costs remain the same.

In marginal costing, only variable costs are considered in calculating the cost of the product, with fixed costs treated as period costs charged against the revenue of the period. The income generated from the excess of sales over variable costs is known as contribution.

2. What is marginal costing in management accounting?

The technique of Marginal Costing represents an improvement over the Absorption Costing technique. According to this method, only variable costs are considered when calculating the product cost, while fixed costs are charged against the period’s revenue. The revenue generated from the surplus of sales over variable costs is technically termed Contribution under Marginal Costing.

3. What is marginal cost in accounting?

The technique of marginal costing revolves around marginal cost. Therefore, it becomes necessary to understand the term ‘Marginal Cost’. The Institute of Cost and Management Accountants in London has defined Marginal Cost. as “the amount at any given volume of output by which aggregate costs change if the volume of output is increased by one unit.” Upon analyzing this definition, we can conclude that the term “Marginal Cost” refers to the increase or decrease in the cost amount due to a single unit’s increase or decrease in production.

You May Also Like:-

Limitations of Management Accounting

advantages of standard costing