Table of Contents:-

- What is asset liability management?

- Asset Liability Management Meaning

- Scope of Asset Liability Management (ALM)

- Importance of Asset Liability Management

- Need for Asset Liability Management

- Components of Asset Liability Management (ALM)

- Organizational Structure of Asset Liability Management (ALM)

- Procedure of Asset Liability Management

- Techniques for Assessing Asset-Liability Risk

What is asset liability management?

The Asset Liability Management (ALM) function strategically plans, directs and manages the flow, composition, and interest rates of a bank’s assets and liabilities. ALM’s responsibilities closely align with the overarching objectives of the bank.

Historically, the banking industry did not consider a detailed ALM function necessary when regulators controlled interest rates and operations focused on transaction volume.

However, with the deregulation of interest rates, increased interest rate volatility, and heightened competition in the financial market, the significance of the ALM function has grown increasingly in today’s dynamic environment.

Asset Liability Management Meaning

Asset Liability Management (ALM) is a strategic financial practice that involves the management of assets and liabilities. It is a risk management technique designed to optimize returns, maximizing profitability, managing risks while ensuring a healthy surplus of assets over liabilities.

ALM takes into account various factors such as interest rates, earning potential, and risk tolerance to effectively balance assets and liabilities. This practice is also commonly known as Surplus Management.

Over the past decade, the definition of Asset Liability Management (ALM) has significantly changed. It is now used in many different ways in different contexts. Asset and Liability Management (ALM), originally developed by financial institutions and banks, is now widely being used in industries too.

Asset-liability management refers to the process by which an institution manages its balance sheet to allow for alternative interest rates and liquidity scenarios. Banks and other financial institutions provide services which expose them to various kinds of risks like interest risk, credit risk and liquidity risk.

Asset Liability Management Definition

Asset liability management is an approach that allows institutions to manage and reduce risks associated with their assets and liabilities. ALM models enable institutions to measure and monitor risks, which helps them to develop suitable strategies for reducing the risks associated with them.

The Society of Actuaries Task Force on ALM Principles, Canada, defines ALM as – “Asset Liability Management is the ongoing process of formulating, implementing, monitoring and revising strategies related to assets and liabilities in an attempt to achieve financial objectives for a given set of risk tolerances and constraints”.

Asset-liability management is the first step of the long-term strategic planning process. Therefore, it can be considered as a crucial component in intermediate-term planning. The various aspects of balance sheet management deal with planning as well as direction and control of the levels, changes and compositions of assets, liabilities and capital.

Scope of Asset Liability Management (ALM)

Asset Liability Management (ALM) is an essential component of a bank’s detailed risk management framework; it aims to reduce various risks that can impact the institution’s financial stability. ALM specifically addresses the following key risks:

1. Liquidity Risk: This risk arises from unexpected fluctuations in cash flows from both assets and liabilities, affecting the bank’s banking and trading books.

2. Interest Rate Risk: This risk arises from fluctuations in interest rates on assets and liabilities held within the banking book, potentially impacting the bank’s profitability and financial health.

3. Market Risk: This risk is driven by price fluctuations in the market, leading to changes in the value of the trading portfolio and exposing the bank to potential losses.

Banks can enhance their financial stability and sustainable growth in a dynamic and challenging market environment by effectively managing these risks through ALM practices.

Importance of Asset Liability Management

The main reasons for the growing importance of Asset liability management – ALM are:

- Volatility.

- Rapid innovations taking place in the financial products of the bank.

- Regulatory environment.

- Management recognition.

Need for Asset Liability Management

Asset liability management is the art and science of analyzing, interpreting and managing the composition of a financial institution’s balance sheet. ALM’s primary focus is on addressing up to four key challenges:

1) Understanding the risks that a bank is exposed to due to the composition of its assets and liabilities. This risk manifests itself through the variability of earnings or the variability in the net economic value of the institution’s equity.

2) Forecast the future composition of the bank’s balance and its risk exposure.

3) Determine and attribute interest-related profits to individual assets or liabilities, business units or activities, through Funds Transfer Pricing.

4) Forecast capital requirements and manage the balance sheet in such a way as to maximize shareholder value.

Components of Asset Liability Management (ALM)

The characteristic of the main product classes that make up the portfolio is to be managed by the asset liability manager. Retail transactions, such as deposits and mortgages, have many implicit or explicit options, such as the option for customers to prepay the principal before it is finally due or to withdraw their money from a deposit account at any time.

This introduces customer behaviour into the modelling of the risks. The behaviour depends on the structure and purpose of the product. The main components of asset liability management are as follows:

The components of Asset Liability Management (ALM) are listed below:

- Bank Assets

- Retail Personal Loans

- Retail Mortgages

- Credit-Card Receivables

- Commercial Loans

- Long-Term Investments

- Traded Bonds and Derivatives

- Bank Liabilities

- Retail Checking and Savings Accounts

- Retail Fixed Deposits

- Deposits from Commercial Customers

- Bonds Issued by the Bank

Bank Assets

The following are the assets of commercial banks:

1) Retail Personal Loans

Retail personal loans may be either fixed or floating rates. If they are floating, they are priced off the prime rate. Fixed-rate loans are generally paid off in equal instalments. The instalments include both interest payments and a partial repayment of the outstanding principal. The amount of each instalment (I) depends on the initial amount lent (L.), the periodic interest rate (r) and the number of periods over which the payments will be made (T). The NPV of the installments must equal the initial amount lent:

$$L=\sum_{t=1}^T\frac I{{(1+r)}^t}$$

This equation can be re-arranged to give the installment amount as a function of L, r and T:

$$\mathrm I=\mathrm L\frac{\mathrm r}{1-\left({\displaystyle\frac1{1+\mathrm r}}\right)^{\mathrm T}}$$

For example, if the annual rate is 8%, a ₹100, the 6-year loan would have annual installments of 21.63. Retal loan agreements generally allow the customer to pay the loan amount back to the bank earlier the originally required. Customers might do this if they had an unexpected windfall or if rates had fallen and they were able to get a replacement loan elsewhere at a lower rate. This prepayment risk is not significant for loans of one or two years but is significant for mortgages.

2) Retail Mortgages

Most mortgages in the United States are fixed rates and have a maturity of many decades. In emerging markets, mortgages tend to be for a shorter term and only fixed for the initial years. This reduces the interest-rate risk for the bank but increases the probability of the customer defaulting on their payments in the event of rising interest rates. From an AL.M perspective, long-term, fixed-rate mortgages could be considered to be simple bonds if it were not for the prepayment option.

To understand the importance of the prepayment option, consider a 100, 10-year bond paying 10% annually, If the current 10-year rate was 10%, the bond would be worth ₹100. If the rates dropped to 55% the bond would be worth 159 and the holder would have gained 59.

$$\mathrm{Initial}\;\mathrm{Value}=\frac{100{(1+10\%)}^{10}}{{(1+10\%)}^{10}}=100\mathrm{Rs}.$$

$$\mathrm{New}\;\mathrm{Value}=\frac{100{(1+10\%)}^{10}}{{(1+5\%)}^{10}}=159\mathrm{Rs}.$$

3) Credit-Card Receivables

Many banks have a large portion of their assets in the form of credit-card receivables, either from credit cards that they have originated or from Asset-Backed Securities (ABS) that are backed by credit-card receivables. Interest payments are typically calculated as a fixed percentage above the prime rate, often with caps on the maximum that can be charged.

The value of credit-card receivables depends on two main factors, the default rate and the difference between market rates and the rate charged on the cards. The most important factor is the default rate, which can be on the order of 10% to 20%. The default rate is generally measured as a credit risk, but it is also possible to model it as an ALM risk in a similar way to the modelling of prepayments for mortgages.

4) Commercial Loans

Large commercial loans are priced based on current market rates, and can therefore resemble bonds in many ways. These loans may also include prepayment options that can be used as effectively as traded instruments.

5) Long-Term Investments

The ALM book includes balance-sheet items as “strategic investments”, which are bought by the senior management as a means of investing the bank’s surplus funds. The ALM book may also include real estate that is used by the bank or owned by the bank as an investment.

Long-term investments, such as equities and real estate, are highly influenced by changes in interest rates. Therefore they should be considered when analyzing a bank’s structural interest-rate position. It can be challenging to accurately model the interest-rate sensitivity of illiquid assets like equities and real estate.

A practical approach is to use market indices as a proxy or develop cash-flow models based on company income and real estate rental rates.

6) Traded Bonds and Derivatives

The ALM book includes liquidly traded instruments, such as swaps, bonds and options. Identical instruments could also be held in the trading book, but the instruments in the ALM book are held either to modify the interest-rate position of the book or as a temporary place to invest the bank’s funds before they are used for customer transactions.

Bank Liabilities

The following are the liabilities of banks:

1) Retail Checking and Savings Accounts

Checking and savings accounts are also known as Demand Deposit Accounts (DDA), Demand deposits such as checking and savings accounts have a contractual maturity of zero because they must be repaid to the customers as soon as they are demanded.

Checking and savings accounts generally earn interest payments that are equal to or close to zero. Customers have DDAs for convenience and cash management. From a bank’s point of view, the profitability of a checking account is the income the bank can make from investing the funds, plus any fees charged to the customer, minus all the administrative costs.

However, checking accounts are demand deposits and can be withdrawn at any time, in practice the total balance for the sum of all checking accounts in a bank is typically relatively stable. The net effect is that the banks can rely on having most of this tiny for many months or years.

However, when interest rates rise, the total balance of checking accounts tends to fall as customers become more careful in sweeping their checking accounts into high-yielding savings accounts.

In general, the value of a liability is the NPV of the cash flow of the liability. In the case of a non-interest-bearing checking account, the cash flows arise from changes in the net balance

2) Retail Fixed Deposits

Fixed Deposits (FDs) are available in various terms ranging from months to years. FDs are also known as Certificates of Deposit (CDs). Fixed Deposits (FDs) are a financial product where customers agree not to withdraw their funds for a given period in exchange for a higher fixed-interest payment.

If the customers withdraw their funds before the agreed-upon time, they will forfeit the interest income. At the end of the deposit period, customers have the option to redeposit or roll over their funds. The new interest rates will be determined by the current market rates.

Fixed deposits have interest-rate characteristics that are similar to floating-rate bonds or short-term bonds. The main difference between fixed deposits and bonds is that the interest rate is not tied directly to the market rate, but is more commonly tied to the prime rate minus a few per cent.

The prime rate is the rate posted by the bank to its retail customers. It is only changed when there is a significant change in market rates and typically changes every one to six months. It is often modelled as a lagged response to changes in the three-month rate.

The prime rate is changed by banks as a response to both the market rates and the competitive situation; the value of fixed deposits is therefore a complex function of the market behaviour, customer behaviour and bank behaviour.

3) Deposits from Commercial Customers

Large deposits from commercial customers are generally priced very close to the prevailing inter-bank rate and are therefore well approximated as bonds.

4) Bonds Issued by the Bank

The ALM book includes bonds that have been issued by the bank. These bonds are occasionally issued by banks to adjust their interest-rate position, raise funds or modify the capital structure. They are a valuable tool for determining the bank’s actual cost of debt.

Organizational Structure of Asset Liability Management (ALM)

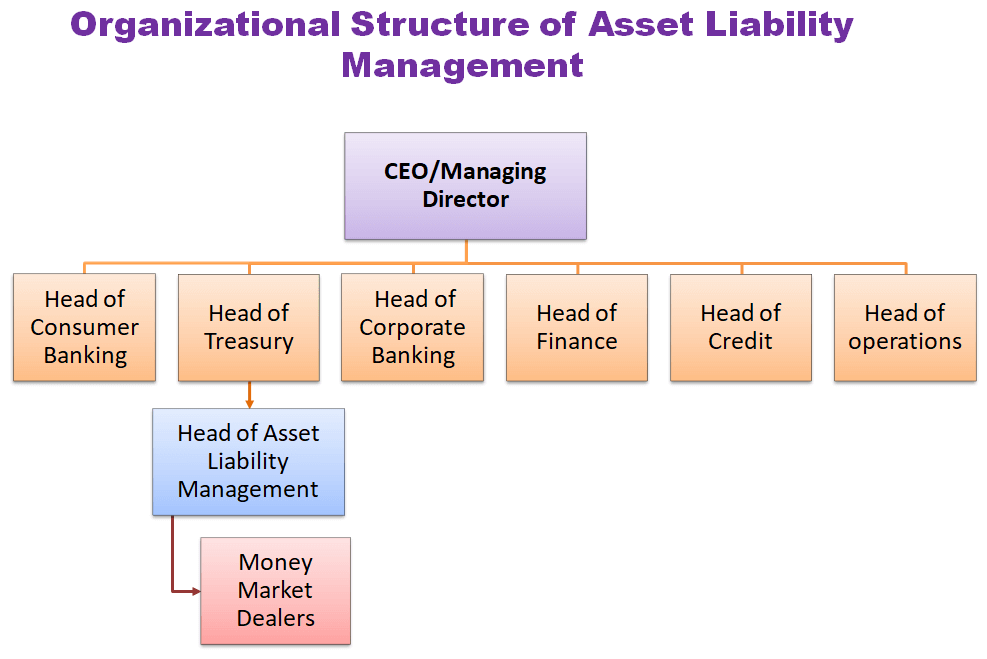

Generally, the organizational structure of ALM is as follows:

Asset Liability Management (ALM) Organization

1) The Board should have overall responsibility for the management of risks and should decide the risk management policy of the bank and set limits for interest rate, liquidity, equity price risks and foreign exchange.

2) The Asset Liability Committee (ALCO) consist of the bank’s senior management including the CEO. The CEO is responsible for ensuring adherence to the limits set by the Board and for determining the business strategy of the bank on both the assets and liabilities sides, in alignment with the bank’s budget and established risk management objectives.

3) The ALM desk, consists of operational staff who are responsible for monitoring, analyzing, and reporting risk profiles to the ALCO. Additionally, the staff is also responsible for preparing forecasts (simulations) that represent the potential impacts of different market conditions on the balance sheet. Based on these forecasts, the staff will recommend the actions needed to ensure compliance with the bank’s internal limits.

4) The Asset and Liability Committee (ALCO) is a decision making unit responsible for strategic balance sheet planning. It focuses on managing risks and returns. To ensure the organization’s financial stability and growth it includes the strategic management of interest rate and liquidity risks.

Each bank must determine the role of its ALCO, its responsibilities, and the decisions it will be required to make. The bank’s business and risk management strategy must ensure that the bank operates within the limits or parameters set by the Board.

Business issues that the ALCO will consider will include product pricing for deposits and loans, the preferred maturity profile of new assets and liabilities, and other relevant factors. The Asset and Liability Committee (ALCO) is responsible for monitoring the risk levels of the bank and reviewing the outcomes and progress in the implementation of the decisions made in the previous meetings.

5) The ALCO would also articulate the bank’s current interest rate view and use this information to inform future business strategies. Regarding the funding policy, for example, its responsibility would be to decide on the source and mix of liabilities or the sale of assets.

To achieve this goal, it will need to establish a perspective on the future trajectory of interest rate fluctuations and determine an optimal funding strategy that balances fixed and floating rate funds, wholesale versus retail deposits, money market versus capital market funding, domestic versus foreign currency funding, and so forth. Individual banks will have to decide the frequency of holding their ALCO meetings.

Procedure of Asset Liability Management

to assess the effectiveness of Asset Liability Management, a thorough procedure must be followed to review different aspects of internal control, funds management and financial ratio analysis. Below is a step-by-step approach for conducting an ALM examination for a bank is outlined.

Step 1:

The bank’s financial statements and internal management reports should be reviewed to assess the asset and liability mix, with particular emphasis on the following areas:

1) Total liquidity position (Ratio of highly liquid assets to total assets),

2) Current liquidity position refers to the minimum ratio of highly liquid assets to demand liabilities and deposits.

3) Ratio of Non-Performing Assets to Total Assets,

4) Ratio of loans to deposits,

5) The proportion of short-term demand deposits compared to total deposits.

6) Ratio of long-term loans to short-term demand deposits,

7) Contingent liabilities for loans as a proportion of total loans,

8) Ratio of pledged securities to total securities.

Step 2:

It is to be determined whether the bank’s management effectively evaluates and plans for its liquidity requirements, as well as whether the bank has sufficient short-term funding sources available. This should include:

1) Analysis of internal management reports on liquidity needs and sources by which these requirements can be met.

2) Assessing the bank’s ability to meet liquidity needs.

Step 3:

The bank’s future development and expansion plans, with a specific focus on funding and liquidity management aspects, have to be looked into. This entails:

1) Determining whether bank management has effectively addressed the need for liquid assets in securing long-term funding sources is crucial.

2) Reviewing the bank’s budget projections for a certain period in the future.

3) Determining whether the bank needs to expand its activities. What are the sources of funding for such expansion and there are projections of changes in the bank’s asset and liability structure?

4) Evaluating the bank’s development strategies and determining whether the bank will be able to secure planned funds and achieve projected asset growth.

5) Determining whether the bank has included sensitivity to interest rate risk in the formulation of its long-term funding strategy.

Step 4:

Examining the bank’s internal audit report regarding quality and effectiveness in terms of liquidity management.

Step 5:

Analyzing the bank’s strategy for addressing unforeseen liquidity needs by:

1) Determining whether the bank’s management has evaluated the potential expenses that may arise due to unforeseen financial or operational issues.

2) Determining the alternative sources of funding liquidity and/or assets is essential for ensuring financial stability and flexibility.

3) Determining the impact of the bank’s liquidity management on net earnings position.

Step 6:

Preparing an Asset and Liability Management Internal Control Questionnaire is essential to ensure the effectiveness of internal controls. The questionnaire should include the following key components:

1) Has the board of directors consistently fulfilled their duties and responsibilities, which include the following:

i) A clear chain of command for making liquidity management decisions

ii) A mechanism to coordinate asset and liability management for making informed financial decisions.

iii) A strategy to identify liquidity needs and the means to meet those needs.

iv) Guidelines for the appropriate amount of liquid assets and other sources of funds concerning financial needs.

2) Does the planning and budgeting process consider liquidity requirements?

3) Are the internal management reports regarding liquidity management adequate in terms of effectively facilitating decision-making and monitoring decisions?

4) Are internal management reports regarding liquidity needs prepared and reviewed regularly by senior management and the board of directors?

5) Whether the bank’s policy of asset and liability management prohibits or defines certain restrictions for attracting borrowed means from bank-related persons (organizations) to satisfy liquidity needs.

6) Does the bank’s policy of asset and liability management provide for adequate control over the position of contingent liabilities of the bank?

7) Is the information provided sufficient for evaluating internal control? Are there any significant deficiencies in areas not covered in this questionnaire that could later impact the effectiveness of controls?

Techniques for Assessing Asset-Liability Risk

Following are the techniques for assessing assets liability risk:

The list of Techniques for Assessing Asset-Liability Risk:

- Gap Analysis

- Duration Analysis

- Stress Testing

- Scenario Analysis

- Cash Flow Matching

- Value-at-Risk (VaR)