Table of Contents:-

- Meaning of Merger

- Types of Merger

- Merger Process

- Reasons for Merger

- Cost Aspects of Merger

- Advantages of Merger

- Disadvantages of Merger

Meaning of Merger

A merger is a combination of two separate companies into one larger company. This strategic move involves a stock exchange or cash payment to acquire the target company. In a merger, the acquiring company assumes ownership of both the assets and liabilities of the merged company.

All the merging companies are dissolved, leaving only the new entity to continue operations. In general, when two firms of similar size come together, the process is referred to as consolidation. However, when there is a significant difference between the size of the two firms, the term merger is used.

According to the Companies Act, of 1956, the term amalgamation includes ‘absorption’. In S.S Somayajula vs. Hop Prudhommee and Co. Ltd., the learned Judge refers to amalgamation as “A state of things under which either two companies are joined so as to form a third entity or one is absorbed into or blended with another”.

Mergers commonly take two forms:

1) Amalgamation: In this form, two entities combine to form a new entity, extinguishing both existing entities.

2) Absorption: In this form, one entity is absorbed into another. The latter does not lose its identity. Thus, at least one entity will inevitably lose its identity in any merger.

Therefore,

X+Y = X, where company Y is merged into company X (Absorption).

X+Y = Z, where Z is an entirely new company (Amalgamation or Consolidation).

Usually, mergers occur in a consensual setting, where executives from the target company collaborate with those from the purchaser in a due diligence process. This process ensures that the deal is mutually beneficial for both parties involved.

What is Merger?

In a merger, the boards of directors of both companies agree to combine forces and then seek approval from their respective stockholders for the merger to proceed. In most cases, at least 50% of the shareholders from both the target and bidding companies must approve the merger to move forward.

The target firm ceases to exist and becomes part of the acquiring firm; for example, Digital Computers was absorbed by Compaq after it was acquired in 1997. The merger of TOMCO Ltd. with HUL is a classic example of absorption.

In a consolidation, a new company is formed after a merger, with the acquiring company and the target company’s stockholders receiving shares in the new entity.

For example, Citigroup was established by consolidating Citicorp and Travelers’ Insurance Group.

Take the example of Asian Paints-Berger International:

1) In 2002, Asia acquired a 50.1% controlling stake in Berger International.

2) The deal amounted to ₹57.6 Crores. Although Berger International had no operations in India, it formed Berger Paints India Ltd in Calcutta.

3) The objective was to enter the Southeast Asian market, including countries such as Singapore, Thailand, Myanmar, Bahrain, Malta, UAE, Jamaica, Barbados, and Trinidad and Tobago.

Types of Merger

Types of Merger are listed below:-

- Horizontal Merger

- Vertical Merger

- Conglomerate Merger

- Congeneric Merger

- Reverse Merger

The 5 major types of mergers are explained as follows:

1) Horizontal Merger

When two or more businesses dealing with the same product or service join, it is a horizontal merger. This type of merger aims to eliminate competition among the various units involved.

For example, when two manufacturers produce the same kind of cloth, two booksellers, or two transport companies operating on the same route, the merger in all these cases would be considered horizontal.

In addition to avoiding competition, there are economies of scale, marketing efficiencies, and eliminating duplication of facilities, among other benefits.

For example, the mergers of Tata Industrial Finance Ltd. with Tata Finance Ltd., GEC with EEC, and TOMCO with HLL exemplify these principles.

A potential merger between Coca-Cola and the Pepsi beverage division is a horizontal merger. Such a merger aims to create a new, larger organization with increased market share.

Due to the similarity in the business operations of the merging companies, there may be opportunities to consolidate certain functions, such as manufacturing, to streamline operations and reduce expenses.

2) Vertical Merger

A vertical merger represents firms engaged at different stages of the production or distribution of the same product or service. In such cases, two or more companies dealing in the same product but operating at different stages may collaborate to streamline the production process.

For example, a petroleum-producing company may establish its petrol pumps to sell its product. A railway company may partner with a coal mining company to transport coal to various industrial centres. Similarly, a textile unit may merge with a transport company to deliver products to different locations.

All these instances are examples of vertical mergers. The underlying idea behind this type of merger is to integrate two different stages of work to ensure speedy production or efficient service. For example, the merger of Reliance Petroleum Ltd. with Reliance Industries Ltd. is illustrative of a vertical merger.

3) Conglomerate Merger

When two companies engaged in entirely different activities join forces, it constitutes a conglomerate merger. The merging companies are not directly related to each other regarding industry or function.

For example, a manufacturing company may merge with an insurance company, while an insurance company may connect with an automobile company.

Although there may be some standard features among merging companies, such as channel of distribution or technology, this type of merger is undertaken to diversify activities.

4) Congeneric Merger

It occurs when two merging firms are in the same general industry. Still, they have no mutual buyer/customer or supplier relationship, such as a merger between a bank and a leasing company. An example is Prudential’s acquisition of Bache & Company.

5) Reverse Merger

A unique type of merger called a reverse merger, is used to go public without the expense and time required by an IPO. In the case of an ordinary merger, a profitable company takes over another company, which may or may not be worthwhile.

The objective is to expand or diversify the business. However, in the case of a reverse merger, a financially healthy company merges into an economically weak company, and the former is dissolved.

The basic philosophy of a reverse merger is to take advantage of the Income Tax Act of 1961 provisions, which permits a company to carry forward its losses to set off against its future profits.

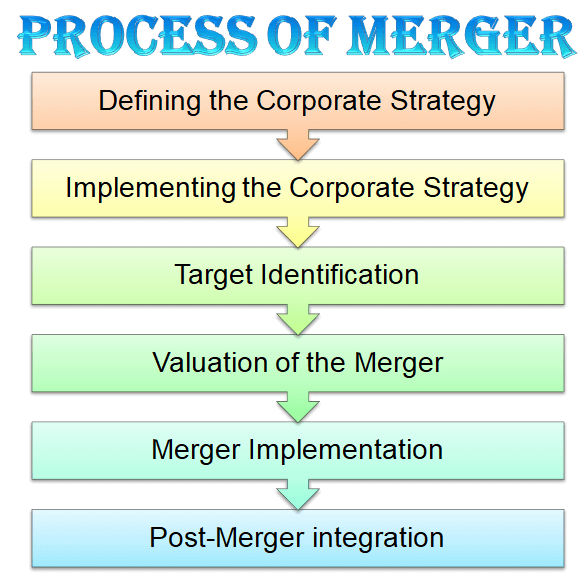

Merger Process

To avoid the pitfalls mentioned above and ensure the success of the merger activity, companies should adhere to a systematic action plan for their merger activities.

The merger process consists of the following stages:

The merger process consists of the following stages:

- Defining the Corporate Strategy

- Implementing the Corporate Strategy

- Target Identification

- Valuation of the Merger

- Merger Implementation

- Post-Merger integration

1) Defining the Corporate Strategy

A firm needs to first clearly define its corporate strategy and determine the business it is currently engaged in. It should consider what business it intends to pursue in the future, how it plans to grow, and how it aims to be recognized.

2) Implementing the Corporate Strategy

Next, the company should define a clear route or roadmap to implement its corporate strategy, whether it intends to use a merger, joint venture, strategic alliance, or internal development as a strategy for its growth or diversification plans.

This stage includes a detailed evaluation of the various alternatives available to the company regarding M&A versus internal development.

3) Target Identification

If the firm finds it attractive to pursue the M&A route, sufficient effort should be devoted to identifying the right kind of target firm to merge or acquire. Parameters for identification should include financial considerations, business strengths, and weaknesses, specific resources, competencies, and capabilities the target firm will bring into the merger, the market power the merger would generate, as well as the effort required to integrate the two firms’ strategies, structures, culture, and processes.

4) Valuation of the Merger

Then, a financial valuation of the merger should commence. The specific cost and premium the firm would be willing to pay for acquiring shares or management control of the target firm would depend on the projected synergies the merger will likely yield.

5) Merger Implementation

Tax, regulatory, and market issues dominate the next stage of the merger process, the implementation phase. During this stage, depending on local laws, conditions, and shareholder preferences, the merger could occur through a stock swap, a tender offer, a cash offer, or any other method.

Issues such as registering the merger, obtaining board and shareholder approvals, making public announcements, and notifying the stock exchanges are necessary for this stage of the merger process.

6) Post-Merger Integration

The final stage, called post-merger integration, includes activities such as asset stripping (selling off those assets in the target company that are not likely to add value to the merged or acquired firm), efforts to improve operating efficiency and establish managerial systems at the acquired firm, streamlining operations of the combined firm to ensure that projected synergies are realized, and initiatives to develop the right corporate culture, provide appropriate management direction and leadership, and ensure the competitiveness of the combined companies.

Reasons for Merger

The merger activities primarily result from the following factors and strategies, which are classified into three categories:

Motives for the Merger are listed below:

1. Strategic Motives

-

- Expansion and Growth

- Diversification Strategy

- Economies of Scale

- Synergy

- Market Penetration

- Market Leadership

- Utilization of Surplus Funds

- Risk Reduction

- New Product Entry

- New Market Entry

2. Financial Motives

-

- Deployments of Funds

- Fund Raising Capacity

- Market Capitalization

- Increase in Value

- Operating Economics

- Increasing EPS

- Lowering Financing Cost

- Revival of Sick Unit

- Better Financial Planning

3. Organizational Motives

-

- Superior Management

- Ego Satisfaction

- Retention of Managerial Talent

- Removal of inefficient Management

The motives behind mergers can be explained in detail as follows:

1) Strategic Motives

The strategic motives of mergers are as follows:

i) Expansion and Growth

Expanding and growth through a merger is less time-consuming and more cost-effective if the government permits. A company may grow slowly through internal expansion. Merger or amalgamation enables satisfactory and balanced company growth at different stages through consolidation.

Growth through mergers or amalgamations is also cheaper and less risky. Acquiring a going concern can reduce costs and risks associated with expanding operations or introducing new product lines. By acquiring other companies, an enterprise can maintain a desired level of growth while minimizing potential challenges.

ii) Diversification

Two or more companies operating in different industries can diversify their activities through amalgamation. Since these companies are already used within their respective industries, there will be less risk in diversification.

When a company attempts to diversify its operations by entering new lines of activity, it may encounter various challenges in production, marketing, and other areas. Some businesses already operate in different industries, so they must have overcome many obstacles and challenges.

The process of amalgamation will combine the experiences of individuals in various activities. Therefore, amalgamation serves as the best method for achieving diversification.

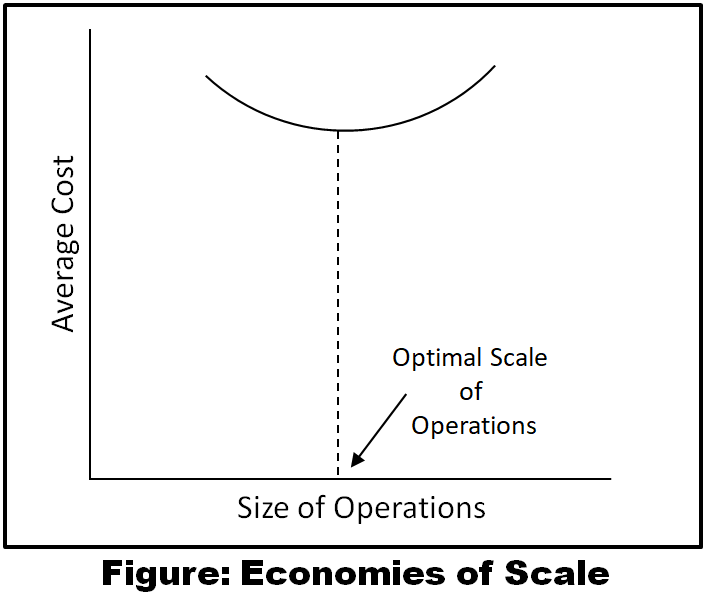

iii) Economies of Scale

A merged company will have access to more resources compared to individual companies. This access will assist the company in expanding its operations and capitalizing on economies of scale. These economies will arise due to more intensive utilization of production facilities, distribution networks, research and development facilities, etc.

These economies will be available in horizontal mergers involving companies operating in the same line of products. This enables companies to use resources efficiently and provides a greater scope for intensifying operations.

However, these economies will occur only up to a certain point of operations known as the optimal point. This point represents where the average cost is minimal. Beyond this point, as production increases, the price per unit will also rise. The optimal point of production can be observed in the figure below:

iv) Synergy

iv) Synergy

The concept of synergy refers to the superior combined value of merged companies compared to the sum of the values of individual units. This concept is akin to one plus one, resulting in a sum greater than two. It arises from benefits that are not solely related to economies of scale.

Operating economies are among the various synergy benefits of a merger or consolidation. Other examples of synergy benefits include:

- Integrating vital R & D facilities from one company with better-organized production facilities from another unit.

- Enhanced managerial capabilities.

- Combining substantial financial resources from one entity with profitable investment opportunities from another.

v) Market Penetration

Traditionally, a company might cater to the middle-class and upper-middle-class segments. Introducing a product for other market segments would be more accessible by acquiring a company with a good market share in the specified segment.

vi) Market Leadership

It is typical for the leading player in a market to acquire the second or third player to maintain its market position. Mergers may enable companies to avoid unhealthy competition when too many players are competing for a limited market share.

A company can better control prices with the combined additional market share, leading to increased profitability. Amalgamation will enhance market access and enable the utilization of expertise in marketing management, allowing for the successful implementation of market strategies.

vii) Utilization of Surplus Funds

A firm in a mature industry may generate a lot of cash but may need opportunities for profitable investment. Such a firm should distribute generous dividends and even buy back its shares. However, most management tends to make further investments, even though they may need to be more profitable.

In such a situation, a merger with another firm involving cash compensation can be a more effective way to utilize excess funds.

viii) Risk Reduction

The merger has the potential to reduce the risk to the shareholders of the involved companies. However, this motive has an inherent weakness within the argument. If the shareholder wants to reduce the risk of their portfolio, they can do so more efficiently as individuals.

ix) New Product Entry

Entering a new product market is a time-consuming effort. Companies with adequate resources will do well in the new product market through mergers and acquisitions.

x) New Market Entry

Advertisement and market promotion activities will be more cost-effective if the organization is in multiple locations. Acquiring a new market from a competitor will necessitate a significant investment. Mergers may offer this advantage.

2) Financial Motives

The following are the financial motives behind the mergers

i) Increase in Value

One of the primary reasons for merger or amalgamation is the increase in the value of the merged company. The value of the merged entity exceeds the combined value of the individual companies involved.

For example, if A Ltd. and B Ltd. merge to form C Ltd., the value of C Ltd. is expected to surpass the sum of A Ltd. and B Ltd.’s values.

ii) Deployment of Surplus Funds

The cash-rich companies always look around to take over cash cash-strapped companies to deploy surplus funds in investible projects.

iii) Operating Economies

Several operating economies become available with the merger of two or more companies. Duplicating facilities in accounting, purchasing, marketing, etc., are eliminated.

The superior management emerging from the amalgamation controls operating inefficiencies of minor concerns. The combined companies are better positioned to use than the amalgamating companies individually.

iv) Revival of Sick Unit

If a viable unit falls ill, a healthy company may consider merging with it to capitalize on the hidden potential of the ailing unit.

v) Increasing EPS

Suppose the bidding company has a lower EPS compared to its target company. In that case, the bidder can increase its overall EPS proportionally more than it currently has if the share exchange ratio is 1:1. This process of growing EPS through acquisition is called “bootstrapping.”

vi) Market Capitalization

The increase in Target Company’s income raises the earnings per share and the market value of the share, subsequently leading to a rise in market capitalization.

v) Lower Financing Costs

Many argue that the consequence of larger size and more excellent earnings stability is the reduction in the cost of borrowing for the merged firm. This occurs because the creditors of the combined firm enjoy better protection than the creditors of the merging firms independently.

If two firms, A and B, merge, the creditors of the integrated firm (referred to as firm AB) are safeguarded by the equity of both firms. While this additional protection reduces the cost of debt, it imposes an extra burden on the shareholders; firm A’s shareholders must support tight B’s debt, and vice versa.

In an efficiently operating market, the benefit to shareholders from the lower cost of debt would be offset by the additional burden they bear, resulting in no net gain.

vi) Better Financial Planning

The merged companies will be able to plan their resources more effectively. The collective finances of the merged companies will be more significant, and their utilization may be more efficient than separate concerns. One of the merging companies may have a shorter gestation period, while the other has a more extended one.

The company’s profits with a shorter gestation period will be used to finance the other company. When a company with a more extended gestation period starts earning profits, it will enhance its overall financial position.

vⅱ) Fund Raising Capacity

The increase in fixed assets and current assets base will improve the fundraising capacity and more working capital finance can be sought from banks and financial institutions. The company can issue shares and other debt instruments to the public.

3) Organizational Motives

Some of the organizational motives that caused the merger are given below:

i) Ego Satisfaction

The financial resources available to the top management of large corporate houses encourage managers to explore the possibilities of a merger. The size of the combined enterprise satisfies the egos of the entrepreneurs and senior managers.

ii) Retention of Managerial Talent

Human resources are considered essential. To ensure senior management personnel’s growth and retain management talent, it may be necessary to consider a merger.

iii) Superior Management

By combining the managerial skills are also pooled together. This will enhance the stability and increase the growth rate of both companies. One of the potential gains of the merger is an increase in managerial effectiveness. This may occur if the existing management team, which is performing poorly, is replaced by a more effective management team.

Often a firm, plagued with managerial inadequacies, can gain immensely from the superior management that is likely to emerge as a sequel to the merger. Another allied benefit of a merger may be in the form of greater congruence between the interests of the managers and the shareholders.

iv) Removal of Inefficient Management

A merger provides a speedy remedy for replacing inefficient management within an organization that possesses, for example, high product strength.

Cost Aspects of Merger

Merger activities are an important part of the corporate sector. These activities are taking place for several reasons. The costs and benefits of a merger activity are different for different companies. This depends on the target company’s size, its present business and customer base and the number of shareholders of the company.

Like any other investment type, a merger can be also termed as an investment. The costs of a merger are related to three factors namely impact of revenue, the cost of dealing and the cost of integration. The cost of a transaction in a merger process is the money that is paid for acquiring the company.

This money can create some short-term problems for the company regarding the cash flow. To handle this crucial part of a merger process, the acquiring companies depend on experienced professionals in the field.

Advantages of Merger

The following are the advantages of mergers:

1) Marketing effectiveness is improved.

2) Security for new products is facilitated.

3) The rate of growth of a concern is increased.

4) Improvement in seasonal and cyclical stability is facilitated.

5) Maximum operational efficiency of a business can be achieved.

6) The business size increases through the merger of two companies.

7) Excess working capital can be effectively utilized in profitable investments.

8) The crisis of a minor concern can be overcome after a merger and consolidation.

9) Modernization, innovation, and research and development methods aid business expansion.

10) Increased profitability and earning capacity of concern occur due to the maximum utilization of resources.

Disadvantages of Merger

The disadvantages of mergers are as follows:

1) Reduced Choice

A merger can lead to decreased consumer choice.

2) Higher Prices

A merger can reduce competition and grant the newly formed entity monopoly power. Due to reduced competition and increased market share, the new company can typically raise consumer prices.

For example, there is opposition to the proposed merger between British Airways, a subsidiary of the parent group IAG, and BMI. This merger would provide British Airways with a more significant share of flights leaving Heathrow, allowing them to set prices at premium levels.

3) Diseconomies of Scale

The new firm may experience diseconomies of scale due to increased size. After a merger, the newly formed, more prominent firm may need help maintaining the same level of control and motivating workers. Employees who perceive themselves as part of big multinational companies may need more motivation to perform at their best.

4) Job Losses

Mergers can result in layoffs and workforce reductions. This is a particular concern if it is an aggressive takeover by an asset-stripping company – a firm that seeks to merge and eliminate underperforming sectors of the target firm.